26 Apr Capital 19 Catch-Up

Weekly Index Movement

S&P500 -2.8%

Nasdaq -3.9%

Aussie All Ords -0.7%

I’m getting a distinct feeling of Deja-vu this week as I write this. Once again US Stocks fell because of a rise in interest rates.

The Nasdaq is now down 18% year-to-date and the S&P500 is down 10.4%

To understand what is happening, all you have to do is look at the Federal Funds Interest Rate Futures. This market tells you what its traders think the US overnight cash rate will be in the future.

The Fed will next meet and announce any rate changes on May 4th.

Last week, Fed Chair Powell, started the selling in equities when he said

“It is appropriate in my view to be moving a little more quickly” …… “I also think there is something to be said for front-end loading any accommodation one thinks is appropriate. … I would say 50 basis points will be on the table for the May meeting.”

Thanks Powell for upsetting the apple cart. No more comments from you for a while, please. This is the same guy that was saying inflation was transitory back in December so he has lost all credibility.

Back to these Fed Fund Futures.

A month ago, the odds of a 50bps rise at the May 4th meeting was 68%. The remaining 32% odds were tipping a 25bps rise.

Now, a 50bps rise is all but certain (99.6%) and there’s even a tiny probability (0.4%) of a 75bp hike.

The following meeting (June 14th) is even worse.

A month ago, Futures put the highest odds (66%) on a 50bps hike in June with the next most likely outcome (30%) being a 25bps hike and the odds of a 75bps hike were just 3%

Now those odds stand at 8.5% chance of 50bps, 91.1% chance of 75bps and even a 0.4% chance of a 100bps bump.

By the end of 2022, futures now put an 89% chance on Fed Funds ending the year between 2.75% and 3.25%.

Until the markets get a better handle on where interest rates are going, this uncertainty will drive more selling.

The good news is the market is pricing more and more into the interest rate story so we are getting closer and closer to the end of this current bout of volatility.

Everyone agrees inflation should moderate here. But that is more to do with high comparison readings for April/May/June of 2021. Maybe Powell was right and short-term inflation is transitory, but what about long-term inflation. What is the market telling us about that?

Well, the 5Year Treasury-Inflation-Protected-Securities are saying that inflation will average 3.4% per year over the next 5 years. This is well above the Fed’s 2% target.

3.4% inflation is a much better measure of where inflation will settle out than the present +8% monthly readings we are getting.

The good news is, in the past, when the Fed Funds Rate has exceeded inflation, inflation expectations began to fall.

This tells us we need a Fed Funds rate over 3.4% to end this present inflation cycle. We might well be getting close to that by the end of 2022. And that news is almost fully priced in by the markets.

Takeaway – For now, continue to play it safe. Focus on Dividends and Value. Avoid Growth. We still favour the energy sector. But we are getting closer to the time to buy growth. For this to happen we need a more certain interest rate environment or moderation in inflation. When we see one of those happen, growth will recover. We are just not quite there yet.

Earnings Deliver the Goods

20% of S&P500 companies have reported Q1 earnings so far. According to FactSet:

- 79% of those companies have beaten Wall Street analysts’ earnings expectations.

- Companies have reported actual Q1 earnings that are an average of 8.1% higher than expectations

This is very good news and just what this season needed.

Going into the Q1 reporting season, Wall Street had a $51.85/share estimate for Q1.

If this level of earnings beats can continue then Q1 will deliver a $56.04 result. That would be brilliant as Q4 2021 was $55.37 so a $56 handle on average earnings would show corporate America is still growing.

The problem is, analysts don’t think the companies due to report can keep up the pace. They have only increased their estimates to $52.57/share.

Full-year estimates are $229.76 for 2022 and $251.66 for 2023.

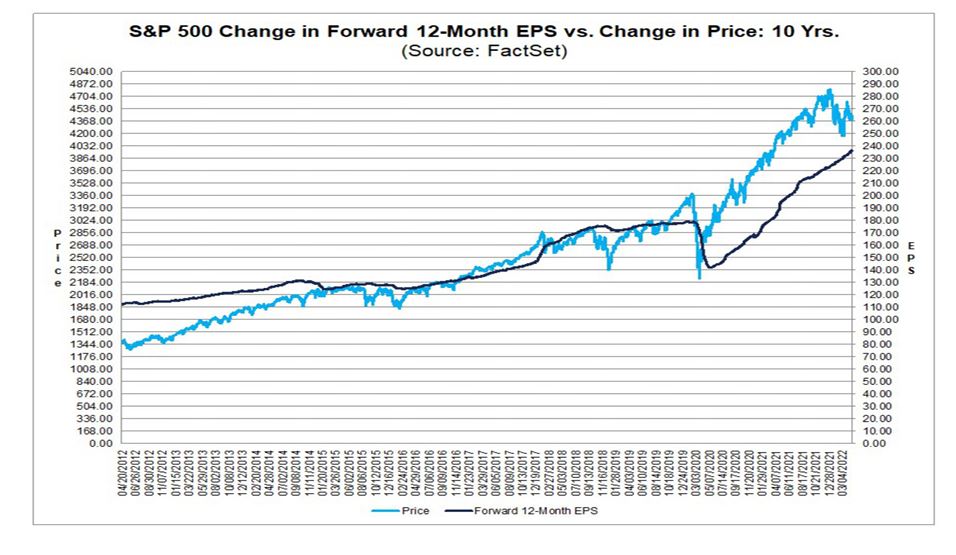

This is very good news for long-term price appreciation. As you can see from this graph from the FactSet research, there is a high correlation between the direction of earnings growth and stock price growth

Takeaway – Growing earnings results in increases to stock prices in the long term. The selling we have had to start this year will eventually turn out to be a great buying opportunity.

Using the VIX to Call Short Term Tops and Bottoms

This is something we first showed in our quarterly webinar update last week.

You can catch a recording of that here if you are interested.

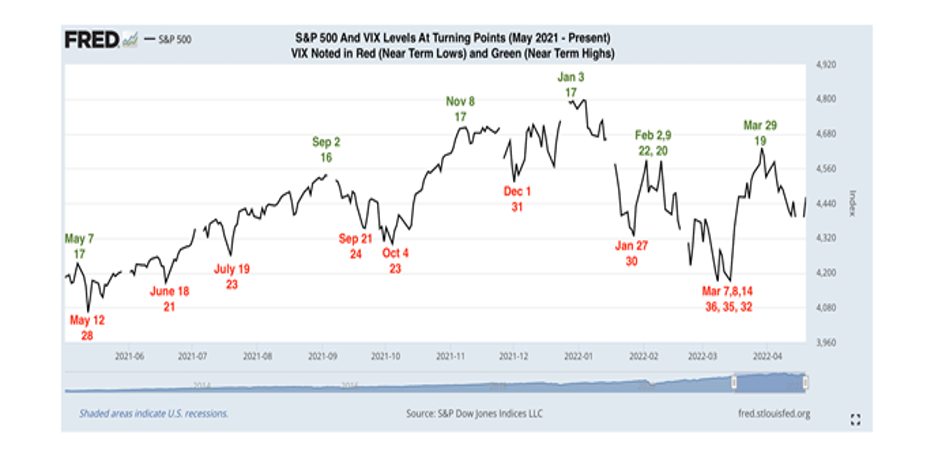

The VIX index is a measure of expected volatility over the short term and is highly correlated with present volatility. It is also referred to as the fear index as high readings in the VIX tend to occur during periods of weakness in stock prices.

We noticed a pattern occurring in the S&P500 around significant short-term highs and lows and what the VIX index was at that time.

Last year, when the VIX fell to 16/17 this coincided with a short-term top in the S&P500. Likewise, a VIX at 23/24 marked a short-term low point.

2022 has been more volatile, so the levels to watch are 20 for a top and 30+ for a bottom.

You can display the VIX on your watchlist in TWS. Call your advisor if you need help adding it in.

During the webinar we highlighted how the VIX had just hit 20 again which has been signifying tops. The market completed an almost 7% fall just after we said this. When stocks were at their lows, around lunchtime in the Monday session, the VIX was at 31.60.

Sure enough, once the VIX got to this level, stocks started to bounce and added 2.3% in the afternoon.

This is a very simple tool you can use to pick tops and bottoms in this market.

Netflix (NFLX) – It’s a B**CH

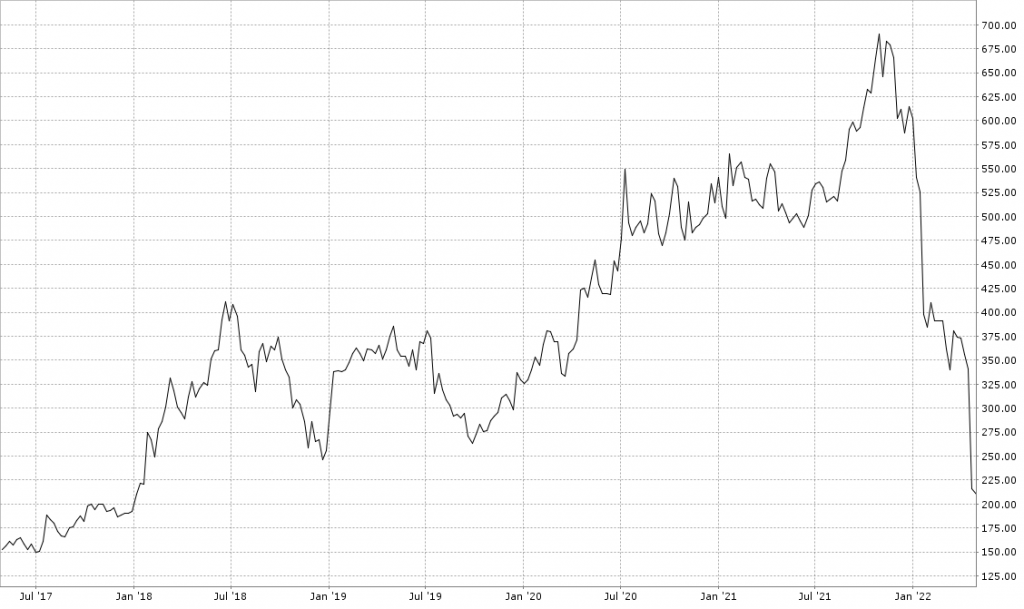

Netflix announced earnings last week and we wanted to use this to highlight a point. In the first three months of 2022, Netflix lost 200,000 subscribers, falling far short of the 2.5 million gain it had projected. It expects to lose 2 million more in the current quarter.

The company’s stock has plunged 40% since the announcement.

“Well, it’s a bitch,” Netflix co-CEO Reed Hastings told employees at a town hall on Wednesday about the decline in subscribers, as reported by the Wall Street Journal.

The problem for Netflix is, it has tied its entire business model to growth. They absolutely must continue to grow the user base. And keep doing it. Or get punished for the slightest hiccup. So they have to keep growing the user base….at all costs.

It is just the way of the world in the high-growth tech sector.

The following is from our “Fundamentals Explorer” in the platform (again ask your advisor if you aren’t sure how to access it)

I want to draw your attention to the Cash from Operating Activities Line which, for each year since 2017 has been

-$1.8B, -$2.7B, -$2.9B, +2.4B, +0.4B

Then the cash flow from Financing Activities for the same period

+$3.1B, +$4.1B, +$4.5B, +1.2B, -$1.2B

Netflix has been financing cash flow through debt and it presently owes $14.5Billion. What happens when interest rates rise this year?

In Q1 of 2022 they spent $555million on marketing. If you back out the 700,000 subscribers they cancelled in Russia, they actually acquired +500,000 subscribers in this period.

Marketing spend was, therefore, $1,110 per acquired customer. Given the average Joe delivers $15 per month in revenue to Netflix, it means Netflix will not recover even their marketing spend for 6 years of a new subscriber.

The business model just does not make sense and we haven’t even discussed the increased competition from all the other providers.

No, Netflix is not one for us.

On the topic of a business model highly leveraged to a growing user base. Anyone remember what happened to Facebook/Meta Platforms (FB) when it announced a decline in customer numbers?

The Coming Week

Tech companies will remain in focus in the coming days as Amazon (AMZN), Apple (AAPL), Alphabet (GGOG), Meta Platforms (FB) and Microsoft (MSFT) all report quarterly earnings this week.

There are no significant economic reports.

Warning

Stock values can go down as well as up. It is possible to lose 100% of your investment in a stock. Any advice given by Capital 19 is general advice only and does not take your personal circumstances into account.