01 May Capital 19 Catch-Up

Weekly Index Movement

| S&P500 | +0.8% |

| Nasdaq | +1.9% |

| Aussie All Ords | -0.3% |

It was a fairly quiet week for economic data.

US GDP came in at only +1.1% verses expectations of +2.0%. Seems growth is slowing, but the fact remains the economy is growing.

That’s exactly what the Fed wants to happen so this wasn’t all bad news.

But the inflation numbers that can be deduced from the GDP number could be worrisome as they came in higher than expected.

What we lacked in economic news was made up for by company earnings announcements. Last week was chock full of them.

Over half of all S&P500 companies have now reported and the results have been strong with 79% of companies beating expectations. This has caused analysts to raise their full-year numbers, which goes a long way to explaining why the index is only 0.2% away from a six-month high.

Let’s take a look at some of these announcements.

Coca-Cola (KO) beat on both revenue and earnings. The company said it benefitted from both price hikes and high demand.

Chipotle Mexican Grill (CMG) beat with comparable sales up 10.9% year-on-year. Margins were up at 25.6% vs 20.7% a year ago. Only one other quarter in the company’s history had a better result on this core metric.

Whirlpool (WHR), a durable goods manufacturer, reported much stronger sales and EPS. Management noted “significant margin expansion”

Takeaway: Companies are using the inflation story to raise prices even when their input costs are not increasing anymore thereby increasing profits. Bad for Powell and inflation but good for company profits.

In the financial space:

PacWest (small bank) reported deposits down slightly but “stabilised in the latter part of March” and “increased by 2.5% in the three weeks since the quarter ended”

CapitalOne (small bank) reported a deposit increase of 5%, loans rose 10% YoY

Visa (V) (used to be technology but has been moved to financials) beat. Payment volumes up 10% YoY recovery in global travel the big winner.

First Republic (FRC) shares were down 75% this week after reporting a loss of $100billion in deposits. Deposits were down 41% QoQ so the Fed has decided to close it down and is looking for bids. At the time of writing, they have not announced a buyer but expect it before the end of the week.

Takeaway: There is nothing wrong with the banking sector. We are seeing a healthy clean out of poorly run companies but no depositors are losing funds. Once this little period ends the sector will be stronger and safer with the riskier banks gone. It is a good thing and nothing to worry about.

Energy:

Sagging energy prices be darned. Exxon (XO) had a blockbuster first quarter. Its profit for the period more than doubled compared to the year-ago period. Indeed, the oil giant’s $11.43 billion in earnings for the first three months of 2023 is a first-quarter record for the company.

Increased production helped beef up the bottom line, according to Chief Financial Officer Kathryn Mikells. “We delivered a first-quarter record despite the fact that energy prices and refining margins are softening a bit,” she told Reuters.

Rival Chevron (CVX) also reported higher profits that topped Wall Street’s expectations, even as profit for its oil and gas production division fell by a fourth compared to the same period a year ago.

Takeaway: Oil companies are still printing money and the big boys are now sitting on massive cash piles. Expect buybacks and also acquisitions of smaller companies which will keep EPS churning higher next year. Both companies also stated they expect higher prices in the second half of the year.

Stay long oil.

Amazon (AMZN) reported an across the board beat. Management noted “much growth ahead” for AWS while advertising was benefitting from machine learning techniques which “delivers unusally strong results for brands”. Revenue topped expectations, and its AWS cloud business posted a 16% increase in sales.

But things turned murkier on the company’s earnings call, as executives offered a somewhat sour outlook on cloud revenue, noting that clients have continued to pare back their spending into the current quarter. “As expected, customers continue to evaluate ways to optimize their cloud spending in response to these tough economic conditions in the first quarter,”

Earnings for Q1 2023 came in at +$0.31 vs a loss of -$0.38 for the same quarter in 2022. But Amazon earnings are always up and down. Revenue is more consistent and that came in at $127bn for Q1 of 2023 vs $116bn for Q1 of 2022.

Amazon has grown revenue by 9.5% in the past year but the stock price is down 40%. Does that sound like a buy to anyone?

Microsoft reported revenues 4% higher than expected. EPS beat by 9% and cloud services reported 27% YoY revenue growth but devices down 30% YoY.

Microsoft earnings were 10.3% higher than last year and the stock is up 7.5% in the same period.

Google’s (GOOG) result was not as strong as Microsoft but still topped estimates. Earnings were down 5% on Q1 2022 as they took a $2.6bn charge related to reduced office footprint

Meta / Facebook (META) topped estimates and returned to growth after 3 quarters of negative sales. Earnings are down 19% on the year but traders are betting we have seen the bottom and the company will return to growth as the stock is up 100% year-to-date.

Takeaway: Corporate America is still working. Company profits are growing despite the glum news and endless predictions of recession. The new bull market started six months ago. Make sure you don’t get left behind.

As today is May 1st that little old rhyme popped into my head. You know the one

“Sell in May and go away”

But are rhymes actually good advice? I crunched some numbers.

Turns out, over the last 40 years, the average return for the stock market from May to August was a respectable 3.2%. The market was higher in 75% of those summer periods

The average for the whole year is 10% so this May-September period makes up a third of this total return. Admittedly this isn’t as good as October-April, but it is hardly a period worth missing.

After deciding nursery rhymes are rubbish I got carried away with Excel sheets and did more crunching.

Since 1982, when the stock market was higher on the year heading into May, it went on to post a full-year gain 89% of the time, averaging an annual return of 12%.

That’s pretty good odds of this year being an up year

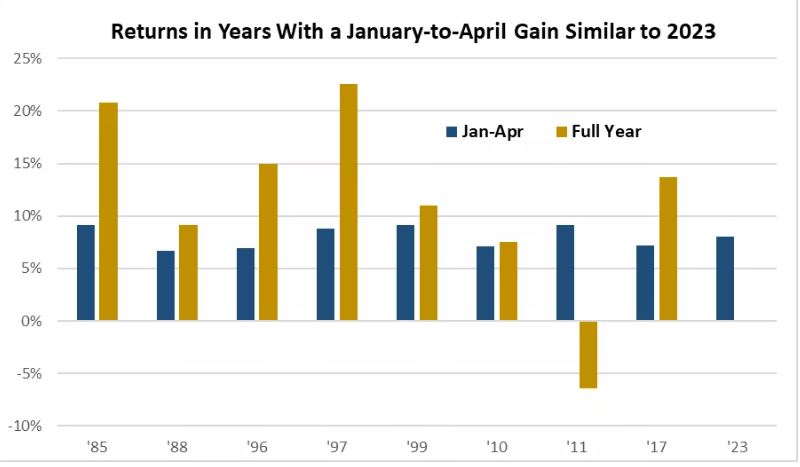

The S&P500 is up 8% so far in 2023. This graphic shows all years where the S&P500 was up between 6.5% and 9.5% going into May and what happened for the rest of the year.

The gold bar (full year) is higher than the blue bar (Jan-Apr) 7 out of 8 years here.

That’s another good sign for more gains to come this year.

The coming week will be another big one. The Fed passes down an interest decision on Wednesday. He will almost certainly deliver +25bps. But it will be the press conference after that will make the difference.

Last time he was a lot more dovish than I expected. This time I think he is going to be more hawkish than the market thinks. I cannot see him confirming market expectations of 2-3 cuts later this year. He will say rates will remain high until they are sure inflation has ended. This will likely see some selling.

But that risk is offset by positive company earnings. of which there will be many next week.

Warning

Stock values can go down as well as up. It is possible to lose 100% of your investment in a stock. Any advice given by Capital 19 is general advice only and does not take your personal circumstances into account and might not be suitable for you.