16 Jul Capital 19 Catch-Up

Weekly Index Movement

| S&P500 | +2.4% |

| Nasdaq | +3.5% |

| Aussie All Ords | +3.8% |

Another great week for global stock markets fueled by low inflation numbers in the US. That lowered interest rate expectations and the Aussie dollar made solid ground against the US Dollar.

Headline inflation came in at +3.0%, but core was still high at +4.8%. Take note Michele Bullock. As the new boss of the RBA if you want to beat inflation you have to act decisively. The US threw several 75bps raises at inflation and smashed it down to levels that stop consumers sweating.

Australian inflation is 7% if you use the official quarterly numbers or 5.6% if you use the new monthly numbers. Either way it needs to come down and that means interest rates up.

This is why the little Aussie battler is finally moving higher against the US. They are just about done raising rates but we still have more to come. That makes the AUD more attractive to hold and so it gains value.

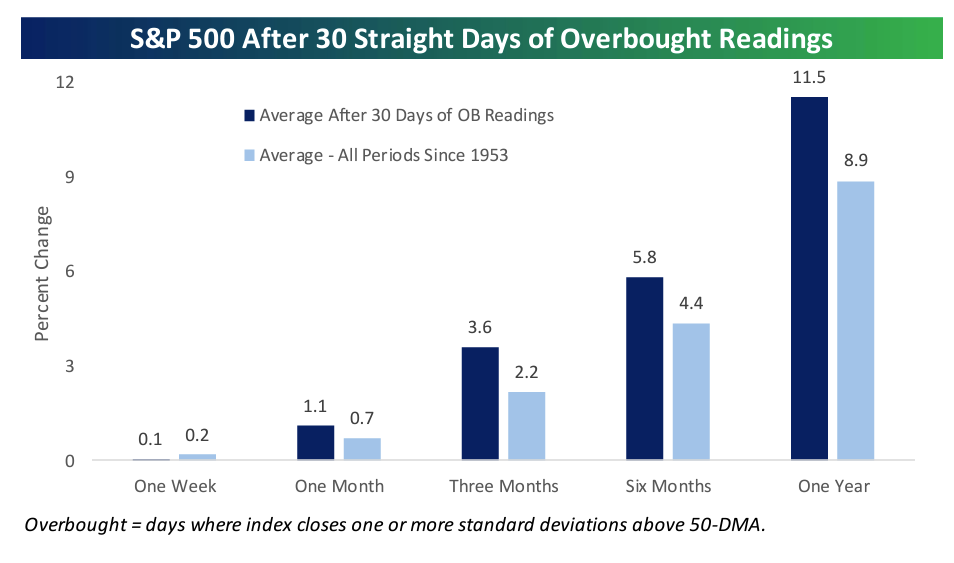

With the market rally chugging along and the S&P 500 making new 52-week highs, the streak of overbought readings (one or more standard deviations above the 50-DMA) has continued. Through Thursday’s close, the S&P 500’s streak has extended to 32 straight trading days. While 32 straight days of overbought readings seems like an extreme, there have been a lot of other streaks of longer durations since the early 1950s when the NYSE shifted to the current five-day trading week. When you hear about the market being overbought, it’s natural to expect a pullback, but as summarized in the chart below, forward returns over the following one, three, six, and twelve months have been better than the average for all periods.

Don’t try and short a bull market, even an overbought one.

After all the talk of inflation and interest rates and recessions of the last 2 years, we can finally put it to bed and get back to focussing on company fundamentals as drivers of stock market returns.

The good news is, companies have just started reporting Q2 so I have something to write about now the big picture stuff is fading.

The numbers reported last week were fantastic

Pepsi (PEP) (a long time holding in our Dividend Growth Strategy) raised its outlook for the year as its results for the second quarter easily beat Wall Street’s expectations. The snack-and-soda giant said its profit and revenue both surged from the same period last year. Still, higher prices for the company’s products hurt demand and resulted in volume declines. Volume, which excludes changes in prices and foreign exchange, dropped 3% for Pepsi’s food divisions and 1% for its beverages. Frito Lay North America volumes did grow, however, as consumers snapped up Doritos and Ruffles.

Delta Air Lines (DAL) posted record quarterly revenue and per-share earnings Thursday, while raising its full-year earnings guidance. Delta is the first U.S. airline to post earnings for the second quarter, and its report should set a strong tone as the industry continues to benefit from sky-high travel demand. Lower fuel prices and demand for premium seats and international travel boosted Delta’s results. The third quarter is looking strong, as well. The company’s outlook for the current period surpassed Wall Street’s expectations. “I think the trends that we’ve seen this year are going to continue,” CEO Ed Bastian told CNBC.

I promised some new ideas for you and something happened last week that gives me confidence on one of them.

ExxonMobil (XOM) has just sealed its biggest deal in six years. Exxon’s got some lofty goals to bring its net emissions down to zero by 2050 – and since it’s not about to cut oil production in any meaningful way, carbon capture is going to be the bedrock of its strategy instead. Now the oil giant is putting its money where its mouth is, with a $4.9 billion all-stock deal to acquire Denbury (DEN). And this isn’t just any acquisition: it’s a strategic move that hands Exxon the biggest network of carbon dioxide pipelines in the US, a crucial piece of the carbon capture puzzle. Plus, Denbury specializes in using carbon dioxide to coax more oil from old oil fields, all while burying more carbon in the ground than the slippery stuff will emit – something seen as a must-have if the world’s going to hit its climate goals.

Exxon wants what Denbury is hoping to build, which is an end-to-end carbon capture, transportation and storage business. By adding these assets Exxon can take care of many of its own carbon emission liabilities and look good doing so. They commented that Denbury offers, “a cost-efficient transportation and storage system accelerates CCS deployment for ExxonMobil and third-party customers over the next decade and underpins multiple low carbon value chains including CCS, hydrogen, ammonia, biofuels, and direct air capture.”

The holy grail of the CCS is the sequestration part, permanently burying it in deep terravaults. DEN has applied to the EPA for permits for sequestration but is behind California Resources (CRC) on this front.

That leads me to CRC.

I’ve been following California Resources Corporation (CRC) for several months.

California Resources (NYSE:CRC) is an energy company based in…you guessed it, California. It operates oil and gas wells with 60% oil, 27% natural gas, 13% NGL’s (no shale, no fracking) with all of its production in California, which believe it or not, is a major strategic advantage. It also owns storage assets and natural gas fired power generation. Lastly, it is one of the largest landowners in the state with associated mineral rights with vast tracks in the Sacramento Basin, the San Joaquin Basin in the Central Valley, the Ventura Basin and Los Angeles Basin.

While the company has good assets, it was overleveraged for years. 2020’s oil fiasco pushed the company into bankruptcy, from which it emerged in January of 2021 with a clean balance sheet, a new management team, and a new board of directors

You might not have heard much of carbon sequestration yet, but you will. Carbon sequestration is basically the removal of carbon from the air. Trees do it naturally. Carbon sequestration as a business involves capturing carbon at its release point (say a power plant) and pumping underground.

You need deep underground caverns for this process. These caverns also need to be of “heavy cap rock” meaning dense rock that doesn’t let the CO2 escape. CRC’s San Joaquin basin assets have heavy cap rock and 1,000 MMT of Co2 storage capacity.

This carbon sequestration could be one of the most environmentally friendly assets and services in California. The company also has identified 5,000 acres as suitable for solar farms.

Last quarter’s operating results were great. Adjusted EBITDAX and free cash flow came in at $204mm and $83 million, respectively. Cash flow could have been higher were it not for drilling activity that was pulled forward into the quarter. Price realisations after hedges were excellent, although still far below the spot market rates seen during the quarter. Oil realized $63.17/BBL, NGLs realized $68.29 and nat gas realised $6.73/mcf. The NGL performance was truly excellent coming out of winter months, and I was encouraged by the strength of natural gas despite the Freeport LNG shutdown.

The company is seeing the same cost inflation other operators are seeing (labor, materials, fuel, etc.) with the average BOE costing $37.76 all in versus $30.72 in Q2 2021. Fortunately, the higher realized prices offset these costs and allow for extremely healthy margins.

Perhaps the biggest announcement of the day was a deal with Brookfield Global Transition Fund, whereby Brookfield committed $500 for 49% of a JV to develop CCS (carbon capture and sequestration). Upon receiving full permits for operation, the company will contribute the assets of CTV1 (Carbon TerraVault1) and Brookfield will invest $500 million with potential incremental investments of >$1 billion. This investment dramatically derisks and provides the bulk of equity funding for the development of the CTV business. In my mind, it legitimizes how real this business can be once the permits are secured and highlights the hidden value within CRC

The company is trading on a PE of less than 4 with a dividend yield of 2.5% and is aggressively buying back its stock at these attractive valuations. It bought back $96 million of stock in Q2 making $360 million at an average price of $39.34 per share since the inception of the program last year. The company added $300 million to this buyback commitment to be completed before the end of Q2 2023.

Given the price Exxon just paid for DEN, I can see CRC easily doubling from here. The DEN/XOM deal potentially puts CRC into play for a major looking for similar carbon capture assets.

Warning

Stock values can go down as well as up. It is possible to lose 100% of your investment in a stock. Any advice given by Capital 19 is general advice only and does not take your personal circumstances into account and might not be suitable for you.