13 Aug Capital 19 Catch-Up

Weekly Index Movement

| S&P500 | -0.3% |

| Nasdaq | -1.6% |

| Aussie All Ords | +0.2% |

After surging for most of the spring and early summer, US markets have taken a breather so far this month. The action has been typical from a seasonal perspective since August has historically been a time of year when the tape is weak, and the action is heavy.

On the economic front, last week was all about inflation.

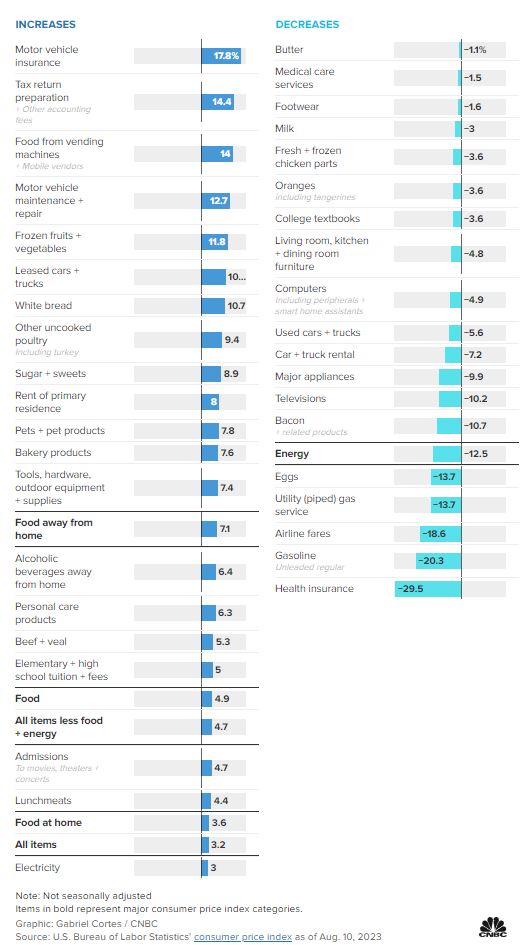

Inflation increased from 3.0% to 3.2% but all of that increase is due to housing. As mortgage rates are so high, people who locked in 3% mortgages in the last few years are reluctant to sell as selling their house and buying another would reset their mortgage to 7%. So they just stay put. That limits supply and keeps house prices high, which in turn leads to this impact in inflation.

It means inflation is unlikely to return to the Fed target soon. That means interest rates will remain high for some time. This is why the 10yr yield is pushing back to prior highs once more. That’s bad news for stocks

Here is the full breakdown of where inflation is happening in the US.

China also announced inflation that shocked the market.

Data out on Wednesday showed that China’s consumer prices fell in July

With over six months of tepid Chinese economic data behind us, July’s dip in prices wasn’t entirely unexpected. And that 0.3% drop from the same time last year was mostly down to food and energy costs taking a hit – with pork prices plummeting a hefty 26%. And sure, if you strip out volatile items like that, then prices actually still climbed. But those staples are a porky part of Chinese households’ expenses, and if they stay weak, falling prices could become a regular fixture in China.

Why should we care?

The mere whisper of deflation sends shivers down economists’ spines. Just ask China’s neighbor, Japan: after the late ’80s property bubble, the nation grappled with persistent price drops. And that meant consumers and businesses clutched their wallets tighter and tighter as time went on, awaiting future bargains – which ultimately caused a spending freeze that wreaked havoc on Japan’s economy and stock market. Spotting parallels between China now and Japan then is easy – from the countries’ aging demographics to their property market ups and downs – so China’s leaders will be desperate to avoid a repeat of Japan’s so-called “lost decades”. But, hey: maybe this data will finally shock them into making some serious economy-boosting moves.

In company news, Commonwealth Bank announced a record profit last week. $10.2 billion. Made as the bank quickly passed on rate rises over the last 12 months and their margin expanded. This profit was a 6% growth over last year.

They increased their dividend too so the full-year payment will be $4.50.

But the result was marred by higher than expected operating costs and growing bad debts.

You know what I think of this bank as an investment. A waste of time. I’ll be surprised if they maintain that level of dividend in the next 12 months as the economy slows. The bank’s CEO recognises this risk

“There were signs of downside risks building as rising interest rates have a lagged impact on mortgage customers and other cost of living pressures becoming a financial strain for more Australians,”

Apple stock has taken a little hit in recent weeks after announcing profits.

It looks to be forming a nice little buying point for those that don’t own it. Yes, revenue was lower than last year but no company can beat every single time. This is just a slow period for them but things could be about to change.

When Apple’s next iPhone goes on sale in September, its upgraded core processor will be more powerful than that of any rival smartphone. That’s possible because of Taiwan Semiconductor Manufacturing, which makes all of Apple’s custom chips. TSMC is using a new process to make smaller, faster and more power-efficient chips, which it refers to as 3 nanometer, for Apple roughly a year before it makes them for anyone else. But that’s not the only thing TSMC is doing for Apple: A sweetheart deal between the companies means TSMC effectively eats the cost of the defects that inevitably crop up in a new manufacturing process.”

I’ve been writing about oil in recent weeks and the value you can find in the sector. The reason I keep hearing not to buy oil companies is because we won’t be using as much oil in future.

Really?

The International Energy Association just released data that shows the world guzzled an average of 103million barrels a day in June. That is and all-time record. Rather than demand falling, we are seeing demand rise.

Oil prices are at a six-month high this week and that means greater profits for oil companies. But it could become a problem for everyone else.

In the latest CPI report, fuel oil was up a whopping 3.0% for the month, even though it crashed 26.5% year over year. Similarly, utility gas was up 2.0% in July but down 13.7% from a year ago. The closely watched gasoline component crashed 19.9% from last year but inched up 0.2% for the month.

The monthly rise in energy subcomponents is not necessarily worrisome by itself. But short-term charts of crude oil, natural gas — and even the entire commodity complex overall — are screaming “bullish” and point to larger potential increases in the inflation statistics in the months ahead.

That’s inflation that could prompt the Fed back into action that the market is not expecting.

Possible worker strikes in Australia helped to spur a surge in European natural gas, highlighting market jitters over potential supply disruptions. Benchmark futures settled 28% higher on a day of extreme volatility that saw the contract top €40 for the first time since June. Workers at Chevron and Woodside facilities in Australia voted to strike, which has the potential to disrupt LNG exports from the country, tightening the global market for the fuel. The exact timing of the industrial action — if it goes ahead — wasn’t immediately clear.

Everywhere I look all I see is more evidence to buy oil companies.

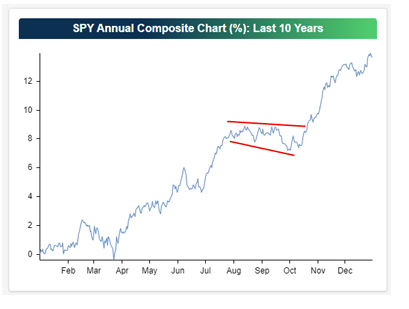

The volatility we have seen in the last couple of weeks is likely to continue through August and September. This is your chance to add to positions on weakness and get positioned for the end of the year. Sideways markets are typical for August and September. You can see that in this chart that shows how prices have moved throughout the year over the last 10 years. It also nicely shows how markets have a tendency to finish the year strongly.

Get your buying lists ready.

Warning

Stock values can go down as well as up. It is possible to lose 100% of your investment in a stock. Any advice given by Capital 19 is general advice only and does not take your personal circumstances into account and might not be suitable for you.