15 Sep 15th September 2025

Index Movement Last Week

| S&P500 | +1.6% |

| Nasdaq | +1.9% |

| Aussie ASX200 | +0.2% |

Bears must be rather miffed here. Investors are looking past bad news, which is a big red flag for pessimists.

Inflation came in a bit higher than expected and employment numbers were a bit weaker. Despite this stocks went up last week.

I’ve been in this game for 17 years now and in that time have come across a few pessimists. They all end up with one thing in common. An investment account with zero dollars in it.

Investing is an optimists game. If you go out there believing everything will be ok in the end, then the outcome is very likely to go that way. Take a look at the markets. Stocks are at all time highs. Again. Betting against this outcome is a fools game.

There is only one thing that really causes a problem for stock markets and that is recession. Outside recession stocks always recover and head higher. There is absolutely no sign of recession at present. Therefore we need to keep buying.

What should you buy?

Shares in businesses with winning secular trends. Secular trends are non-cyclical and play out over years, even decades.

Take cloud computing. Amazon Web Services started in 2002 when Jeff Bezos realised other companies would pay hefty monthly fees to rent the spare computing and data storage capacity Amazon.com had accumulated while building its online store.

AWS has continued to grow and add value each year despite financial crises, a global pandemic and other events. Cloud computing is a durable secular trend.

As is AI. We are just at the start of this new secular trend and there are many years of gains to come from it.

Investors know this which is why Oracle (ORCL) had such a big move last week.

The stock exploded 38% higher on an earnings result last week. It added $255billion in market-cap. To put this in context, that value is more than the total of all the stocks in the S&P500, minus the top 33. It is larger than the market-cap of names like McDonalds (MCD) or American Express (AXP)

It wasn’t the earnings number than produced this reaction. Earnings were actually slightly worse than expected. Rather, it was management projection for it Cloud Infrastructure department. Management sees revenue for that segment growing from $10.3bn in the latest fiscal year to more than $140bn over the next 5 years.

They also disclosed “four multi-billion-dollar contracts with three different customers” driving remaining performance obligations (a measure of backlog) to $455bn. That is another way of saying “we have made these sales and this money is coming in over the next few years”

Companies are spending big on data centres to run their AI models and there is no sign of a slowdown in spend.

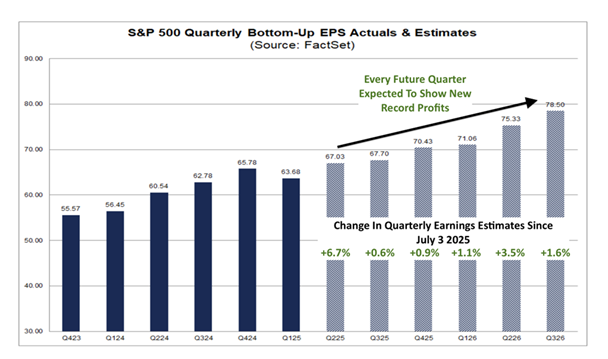

Future Earnings

FactSet produced a nice piece for us again this week. They compiled future earnings expectations for all the stocks in the S&P500 and drew a nice little chart to show how earnings as a whole are expected to grow

Analysts now expect the S&P to post record earnings every quarter over the next year.

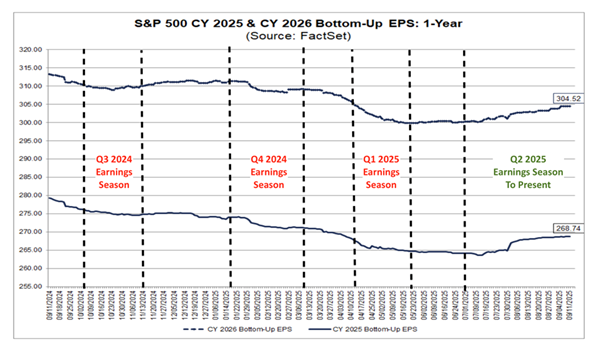

Another interesting chart was this one, which is changes to earnings revisions.

It is highly unusual to see analysts INCREASE earnings estimates for the coming quarter. They normally bring estimates down as the quarter goes on. You can see this in the chart above with the generally down sloping line. Analysts tend to start off too optimistic and then bring the estimates down over time. The fact they are now increasing their estimates is remarkable.

When you take these two charts together it helps us to understand why investors are still willing to buy stocks, even though valuations feel a little stretched right now.

PE’s are high, but if the forecast for the E bit of that is increasing then it means stocks are far from overvalued and can be bought.

So stick at it and keep buying.

Warning

Stock values can go down as well as up. It is possible to lose 100% of your investment in a stock. Any advice given by Capital 19 is general advice only and does not take your personal circumstances into account and might not be suitable for you.