22 Jul 22nd July 2024

Weekly Index Movement

| S&P500 | -2.0% |

| Nasdaq | -4.0% |

| Aussie All Ords | +0.0% |

Last week I said a rotation into small caps had begun and it would be a good time to look at our Top 30 Strategy. It is still up 8% this month despite the sell off this week.

A look at the performance of major US indices this week and on a month to date shows one of the most uneven performances I can remember in some time. While large cap-oriented indices plunged nearly 2%, small caps surged 2%. Between growth and value there was also a similar disparity among large caps, but in the small cap space, both value and growth were up over 1.8, illustrating just how strong the impulse was to buy small caps.

I wrote this next bit on Tuesday last week, in preparation for today’s release. Had I known how timely the piece was to be, I would definitely of published immediately, but it does show how history does tend to repeat in markets…..it just doesn’t repeat exactly………

It has been a great summer for the bulls. The S&P500 is up over 8% in the last two months alone. The question is, can it last?

Seasonality is far from the only factor that impacts markets, but from that perspective, bulls will be swimming against the tide for the next three months.

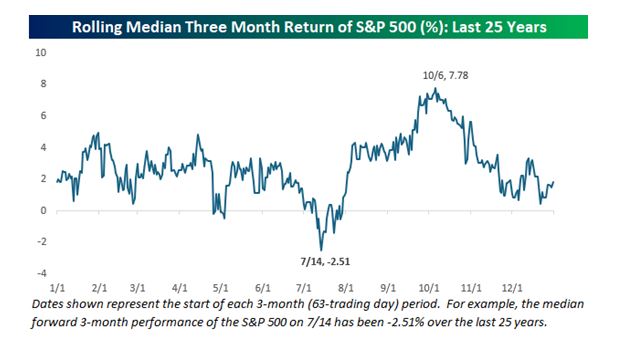

The chart below is a little confusing to read, but what it shows is the average future 3 month return for any date in the year, based on the last 25 years data.

What it says is, if you invested on July 14th every year, and held for 3 months, then your average return would be -2.51%. Conversely, buying on October 6th and holding for 3 months, gives an average return of close to 8%.

Basically, it is saying that we have now entered what is generally the weakest 3 month stretch of the year. The good news is, after this 3 month period ends, we will get the generally best 3 month period.

After such a strong run and entering the weakest times of year………it might be time to take some money off the table, or certainly not add to positions for a bit.

Between Wednesday and Friday the S&P500 dropped 2.9% and the Nasdaq dropped 4.2%. There was no real catalyst for this, except the markets were sitting at an overextended position. After moving up by 8% in 2 months, a 2% drop this week is nothing to be concerned about. It’s a simple reversion to the mean as Greg here would say. He does love a reversion trade does our Greg.

Here is what it looks like on a longer term basis

Nothing to get excited about. Just normal market behaviour.

We trade a lot of options here at C19 so are always looking at the VIX index. In a bull market (like this one) we have 19.5 as a time to buy stocks. VIX is presently at 16.5 so we wouldn’t be rushing in just yet. Wait for a bit more selling before snapping up some bargains.

If you are thinking we are in a bigger mess then wait for a VIX of 27 (1 Standard Deviation).

My view of this recent selling is, it is very constructive. It has mainly been centred on the high-flying big tech names. Whilst the rest of the market has been bought. Rather than this event being a period of selling, it is purely profit taking from the high-flyers and buying into value. A typical bull market rotation. But because the index is so heavily weighted to large Tech, the index comes down. But an index is not a great representation of the whole market these days.

This graph shows this point nicely

We are now about 2 weeks into earnings season and 18% of S&P500 companies have reported. During earnings season I pay particular attention to FactSet and their weekly earnings reports.

FactSet tells me that revenues are looking good but earnings are mediocre so far. But I think this will improve as we get deeper into the season and the tech boys start showing what they can do.

FactSet had the following this week which also helps explain what is happening.

Three points on this data

- The first quarter of the year saw all the S&P’s year over year earnings growth (5.9 percent) come from just these 4 Big Tech companies. The rest of the index showed an aggregate annual earnings decline of 1.2 pct.

- In Q2, the Street is looking for “rest of S&P” earnings growth to turn mildly positive (+5.7 percent), but the Big 4 are still delivering 56.4 pct growth. Their contribution is the reason the index as a whole is expected to post near-double digit (9.7 percent) earnings growth this quarter.

- In Q3 and Q4, Big 4 Tech is still expected to show outsized earnings growth (+28.4 percent), but “rest of S&P” growth should accelerate in Q4 to +15.6 pct from 5.2 pct in Q3. That improvement is why the Street is looking for 17.0 percent year of year index earnings growth in Q4, up from 7.4 pct in Q3.

This is all good news for stocks as it means the bull case for higher prices rests on broad-based earnings improvements, not just strong results from a handful of companies.

It will make picking winners a lot easier as the year progresses.

More good news for stocks last week came from the Federal Reserve.

Chair Powell was interviewed last week at the Economic Club of Washington. Powell described the labor market as “essentially no tighter than pre-pandemic”. The last three “pretty good” inflation readings mean “more progress on inflation” was made in the second quarter, and “do add to confidence” that inflation is headed back to target.

While Powell declined to “send signals today on any particular meeting”, and therefore implicitly ruled out a July cut in two weeks, his discussion of inflation does set up a July meeting that will send a clear signal for a September cut. Powell noted that the FOMC “usually go into FOMC meetings knowing the likely outcome”.

Basically he just told us….”expect rate cuts in September” with more to follow.

Putting all this together, Bulls are still well in charge despite last weeks little bout of selling. Even though things might be a bit tougher for the next couple of months, we will not be seeing significant falls and any pull back in a stock is just a buying opportunity. The market should finish the year higher than where it is now.

Lastly this week I feel I should comment on Biden pulling out of the presidential race. He will see his term out but he will not run for re-election. We don’t know yet who the Democrats will put in his place. Most likely it will be Kamala Harris, but not definitely.

The market has not moved at all on this news today so clever money says “mey” to the news and you should too. Odds of a Trump victory have reduced but he is still the favourite to win.

There is nothing to fear or even get excited about for this election. It is all just business as usual.

Warning

Stock values can go down as well as up. It is possible to lose 100% of your investment in a stock. Any advice given by Capital 19 is general advice only and does not take your personal circumstances into account and might not be suitable for you.