25 Nov 25th November 2024

Weekly Index Movement

| S&P500 | +1.7% |

| Nasdaq | +1.9% |

| Aussie All Ords | +1.1% |

With few economic announcements last week the only item of note was the release of earnings by Nvidia which is now the world’s most valuable listed company.

NVDA delivered record revenue of $35.1 billion, up 94% YoY, fueled by a 112% increase in data center revenue to $30.8 billion. The numbers really are quite phenomenal. The are due to release their next generation AI chip soon, the Blackwell chip and their CFO had this to say about it

“Last week, Blackwell made its debut on the most recent round of MLPerf training results, sweeping the per GPU benchmarks and delivering a 2.2x leap in performance over Hopper. The results also demonstrate our relentless pursuit to drive down the cost of compute.”

AI users want more speed to be able to deliver more applications and with the ability to switch software almost instantly the developers need the fastest chips so customers choose their product. All developers must therefore upgrade or be left behind. And upgrades mean more sales for NVidia.

As amazing as the revenue growth numbers are, the true value in NVidia lies in its 73% return on capital.

To understand why, lets do a hypothetical: Which of these two companies would you prefer to own

- A company with a fixed 5 percent return on capital growing earnings at 20 percent per year

- A company with a fixed 20 percent return on capital growing earnings at 5 percent per year.

The answer is the second company because its return on capital almost certainly exceeds its cost of capital. Even with just a 5% growth rate it will have enough cash flow to invest in the future, pay dividends and buy back stock.

The first company has something wrong with it. A fixed 5 percent return on capital certainly does not cover its cost of capital. To put this another way, would you give your capital to this company to earn 5% on it when you could get very similar returns by leaving it risk free in the bank? Why then buy the stock?

Tech investors have a reputation of rewarding high growth in revenue, but NVidia is showing them the best path to dominance is to have BOTH. High growth in revenue and high return on capital will lead to outsized stock gains.

Now, the only thing to do is go and find another company that is doing both. The problem is, very few of them exist.

Nvidia might well be a unique case study, but it is only the Tech space that can deliver growth and return on capital at outstanding levels. Which is why it is the only sector worth bothering with for growth.

Horizon Oil (HZN – ASX)

Here is something for you income investors out there.

Horizon is an Australian oil and gas producer spitting out cash. It is sitting on a PE of just 8 and has a dividend yield approaching 16% (no franking though).

They have oil producing assets in Australia, New Zealand and China and the number of barrels of oil produced were 19% higher than last year. Profits were down slightly overall because the oil sale price was lower, but that bit is out of their control.

I often write it is a good idea to hold some oil assets in your portfolio as a hedge against inflation and here is one that pays you 15% to do so.

Zeta Global (ZETA – Nasdaq)

Zeta is a marketing company that says it uses AI to develop intelligence on consumers to help its own customers increase sales. “We believe our actionable insights derived from consumer intent enable our customers to acquire, grow and retain consumer relationships more efficiently and effectively than the alternative solutions available in the market,” says Zeta.

The company says its Zeta Marketing Platform can use “machine learning algorithms” to analyse billions of data points to predict consumer intent. Then it can analyze the impact of marketing campaigns, so Zeta customers can tweak them to make them more effective.

Sales trends seem to confirm that these are more than just exaggerated marketing claims.

Zeta has produced eleven straight quarters of greater than 20% revenue growth. Its customers include over 40% of the Fortune 100 companies.

Back on November 11, Zeta reported 42% sales growth. Revenue per customer increased 33%. Cash flow advanced 51%. Earnings loss per share narrowed to $0.09, compared to a loss per share of $0.27 in Q3 2023. The company raised Q4 sales growth estimates by $32 million at the midpoint to $293 million to $297 million.

In short, a classic mid-cap growth play. Shortly after earnings the stock was trading around $36.

Then along came Culper Research with a report titled “Zeta Global Holdings Corp (ZETA): Shams, Scams, and Spam.” The report basically questions the accuracy of the reported financials by ZETA.

The short seller reports are becoming popular. For you and me, we have little ability to influence the outcome of our stock investing. We buy a share (or in this case they sold it short) and then can’t do much to push the price around.

But Culper Research can. Or rather, they can try. They can build a short position then release a scathing report to the market and let everyone else sell down the share price, thereby “talking their own book” and influencing the outcome of their trade.

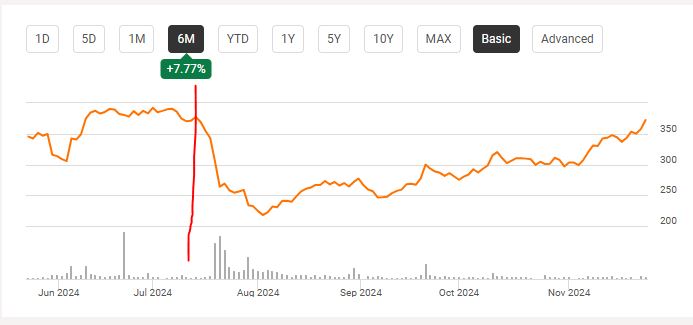

The stock promptly fell to around $18 and has since come up slightly to $22.

Zeta promptly responded that the report was “riddled with misrepresentations, speculative conjecture, and categorically false statements. The report is misleading and conveys, at most, a superficial understanding of Zeta’s business and practices. It relies heavily on questionable sources that get basic facts wrong, cites financial metrics that are off by hundreds of millions of dollars, and doesn’t even correctly identify the Company’s Big Four auditor.”

Last week the company also hosted an investor briefing to publicly answer questions from analysts. They wouldn’t do this if they were not confident the short seller report had it all wrong.

Additionally, Directors have bought stock on market. This is unusual. Normally Directors receive stock as part of their salary package and sell stock every now and then to buy another Ferrari or Lear Jet. For a Director to take his own cash and put it back into the company it takes a big conviction in higher stock prices to come. And who knows the most about what is happening within a company?

I smell a nice opportunity here for a 50% or so profit. All these short sellers will have to buy the stock back to close their position. In addition you will have bargain hunters (like me) looking at this as a steal. (ZETA directors agree with me). It is very hard to put a timeframe on how long it will take for everyone to forget Culper Research. But if what happened to Crowdstrike is anything to go by, the answer is not too long. The red line below is when Crowdstrike went down and stop access to all kinds of systems worldwide.

Of course the risk is the research report is right. But the actions of the company after the release of the report makes me think otherwise.

This Week

On Thursday the world’s population of Turkeys will take a hit as the US stops to consume a huge amount of them for Thanksgiving. Markets will be closed and will also only do a half day on Friday. With little else on the agenda, it will be a quiet week.

Warning

Stock values can go down as well as up. It is possible to lose 100% of your investment in a stock. Any advice given by Capital 19 is general advice only and does not take your personal circumstances into account and might not be suitable for you.